After what I consider a pretty successful first full year of options trading, a new year brings a time to look back, tweak things, and set goals and procedures for the next year.

My goal for 2014 is pretty simple, I would like to generate 45K in options/short term capital gains this year. This will take some smart trading, along with adding additional capital to my account by saving more, but I think it can be done. I would be very suprised if I'm at 20K by June, but think I can play catch up the second half of the year as that's when the seasonality of my job allows me to stash more cash away. So there you have it, one singular "goal". 45K or bust.

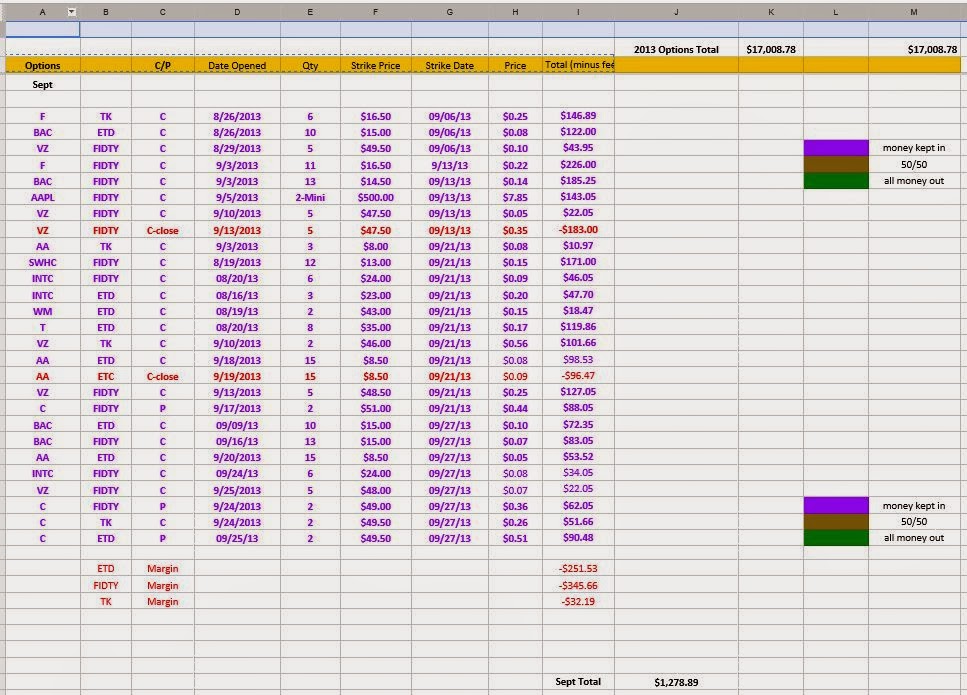

That being said, I am going to change up my rules of engagement a little bit. This year I really didn't follow any protocol with my "earnings" from the options. Some I would simply leave in the account, at other times I would pull out and use as disposable income, there really was no rhyme or reason to what I did with the earnings. So here is a system I have devised to follow this year.

1. I will split the money I earn on options that expire worthless 50/50. 50% will stay in the account, and 50% will be pulled into my banking account. Dividends collected on stocks I own with options on them will for the most part be auto-dripped into additional shares. The few stocks I own that I don't auto-drip will be split in the 50/50 ratio as well.

2. From there I will use the 50% of the money transfered to my bank to pay off whatever debt I would like to target. I currently have a balance on a credit card I would like to clear up (gets close then I seem to put another purchase on it), a new car payment, and the ever present college loans. Applying this extra income to those balances should accelerate the payment pay off schedule, and hopefully get the credit card and the car (almost) paid off by the end of the year.

3. The other 50% I will tally at the end of the month, and initiate a monthly purchase into a dividend growth stock I may own already or start a new position in a stock I want to own (in the TradeKing account I am trying to actively grow), thus generating more income with a potential for capital growth.

By following these steps, I will be paying down debt as well as investing for the future at the same time, and I think this could be a very efficient strategy. It will add a little more book keeping on my end at the end of each month, but I think as I see the balances go down on the few debts I do have, it will keep the motivation up.

So there you have it, my game plan, and now that it is written down, it's just a matter of following the steps every week the options (hopefully) expire worthless. Let the games begin!!